The same five mistakes, on policy after policy

The same coverage gaps show up on action-sports policies again and again. Not because operators are careless. Because the insurance industry has done a poor job explaining the gap between what a policy says and what it pays. Each of the five mistakes below has a predictable ending: a claim arrives, the carrier points at a clause, and the operator writes a check.

This is the version of "check these five things" we would hand any paintball, axe-throwing, trampoline, or family-entertainment operator before their next renewal.

Mistake 1: Assuming General Liability covers your participants

This is the most expensive assumption in action sports. General Liability covers third-party claims: a spectator, a vendor, a parking-lot visitor. Your paying participants are not third parties, and most standard GL policies carry the ISO athletic-participants exclusion, form CG 21 01, which removes coverage for bodily injury to anyone participating in the sport you sponsor.

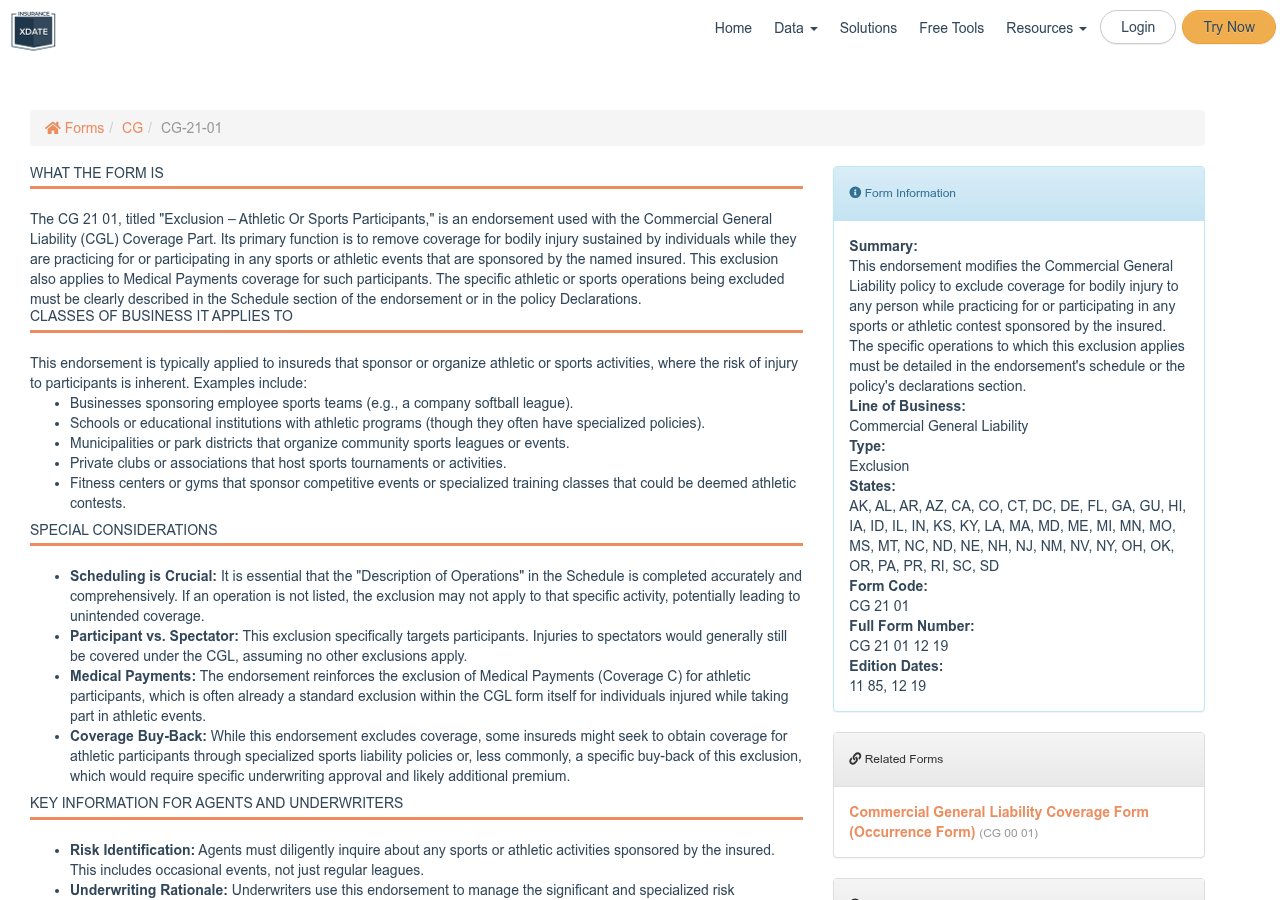

Reference source · Standard ISO exclusion form

ISO Commercial General Liability form CG 21 01, the Athletic or Sports Participants exclusion. When attached, it removes coverage for injury to participants in the sport the business sponsors.

If you have never asked your broker to confirm, in writing, that your policy includes Participant Accident and Participant Legal Liability coverage, ask today. The full breakdown of how this exclusion works is in our guide to the coverage gaps a generalist agent will miss.

The operator who calls me after a denied claim almost always says the same thing: I had a million dollars in liability coverage. They did. They also had the participant exclusion attached to it, and the injured customer was a participant.

Bobby Sharp, Action Sports Practice Lead, Specialty Insurance

Mistake 2: Buying the cheapest policy on the table

The cheapest General Liability policy for an action-sports business is almost always cheapest for a reason: it excludes the exposures that make the business expensive to insure. Participant exclusions, activity limitations, sub-limits, and narrowed coverage definitions are how a carrier prices a policy down.

The policy that looks like a bargain at renewal is often the policy that produces a denial at claim time. Price is a real factor, but on an action-sports account, the cheapest quote and the broadest quote are rarely the same quote, and the gap between them is where the uncovered claim lives.

Mistake 3: Not updating coverage when the operation changes

When an operation changes, the policy does not change with it automatically. A new activity, a second location, private events, a food or bar component, a mobile arm: each is a new exposure, and a policy written before the change may not respond to it.

Mid-term endorsements exist for exactly this reason. The rule is simple: notify your broker when the operation changes, not when the claim arrives. An undisclosed exposure discovered at claim time is a denial waiting to happen.

Mistake 4: Skipping the umbrella

Umbrella and Excess Liability coverage is consistently underused in action sports. It sits on top of the primary policies and extends the limit when a single serious claim threatens to exceed it.

Excess liability provides an additional layer of coverage above existing liability limits for the large, unexpected events that can be catastrophic for a business. For a business with high participant volume and physical-activity exposure, the umbrella is not a luxury. It is the coverage that keeps one serious claim from reaching the operator's assets. The incremental cost of $1M to $2M of umbrella over primary limits is typically modest against the protection it buys, a point we made concrete in our family entertainment center underinsurance case.

Mistake 5: Never reading the exclusions

Exclusions are where coverage ends. Most operators read the Declarations page, the one-page summary of limits, and never read the exclusions that carve pieces out of those limits.

A policy with a broad coverage grant and a long exclusions list can be far narrower than it looks. Ask your broker to walk you through the key exclusions that apply to your class of business: the participant exclusion, the outdoor-structure exclusion, the products sub-limit, the premises-only restriction, the assault-and-battery exclusion. Each one has produced a denied claim on someone's policy.

Read the exclusions before you read the limits. The limit tells you the most a policy can pay. The exclusions tell you whether it pays at all.

Bobby Sharp, Action Sports Practice Lead, Specialty Insurance

The five mistakes at a glance

| Mistake | What it looks like | What it costs |

|---|---|---|

| GL assumed to cover participants | "I have $1M in liability" with CG 21 01 attached | A denied participant claim |

| Cheapest policy bought | Lowest quote, narrowest form | The gap shows up at claim time |

| Coverage not updated | New activity or location, old policy | Undisclosed-exposure denial |

| Umbrella skipped | Primary limits only | One large claim reaches your assets |

| Exclusions never read | Dec page read, exclusions skipped | A carve-out nobody knew about |

"Specialty Insurance has been an incredible foundation for our business. They are personal, professional, and easy to work with."

Ballahack Airsoft LLC

Verified customer review

How to fix all five before your next renewal

The fix is a single review, done with the right kind of broker, well before the renewal date.

- Pull the full policy, not the certificate. Find the words "participant," "player," or "recreational sports participant." If they are not there as covered, you have Mistake 1.

- Compare your quote against one other specialty quote. If your policy was the cheapest, confirm what was excluded to get there.

- List every activity, location, and revenue line you run today. Anything not on the policy is Mistake 3.

- Ask for an umbrella quote. $1M to $2M of excess is usually modest. Decline it on the numbers, not by default.

- Have your broker read the exclusions to you, out loud. If they cannot, that is its own answer.

Work with a broker who places action-sports and specialty-entertainment risk every day, not occasionally. A specialty broker knows the policy language, the exclusions, and the carriers that write the class correctly. The difference shows up in coverage, not just price.

Frequently Asked Questions

Does general liability cover injuries to my customers during the activity?

Usually not. Most standard GL policies carry the ISO CG 21 01 athletic-participants exclusion, which removes coverage for participants in the sport you sponsor. Participant Accident and Participant Legal Liability coverage close that gap.

Is the cheapest action-sports insurance policy a bad idea?

Not automatically, but the cheapest quote is often cheapest because it excludes participant injury, sub-limits key exposures, or narrows coverage definitions. Compare what is covered, not just the premium.

Do I need to tell my broker when my operation changes?

Yes, before the change takes effect. A new activity, location, event line, or food and bar component is a new exposure. An undisclosed exposure can be denied at claim time. Mid-term endorsements exist to keep coverage current.

Is umbrella insurance worth it for an action-sports business?

For most action-sports operators, yes. A single serious participant claim can exceed primary limits, and $1M to $2M of umbrella coverage is typically modest in cost relative to the protection it provides.

What exclusions should I check on my action-sports policy?

At minimum: the athletic-participants exclusion, the outdoor-structure exclusion, the products-liability sub-limit, the premises-only restriction, and any assault-and-battery exclusion. Ask your broker to walk through each one.

Sources

- ISO Commercial General Liability form CG 21 01, "Exclusion: Athletic Or Sports Participants." insurancexdate.com

- Specialty Insurance. The Action-Sports Coverage Gaps a Generalist Agent Will Miss

- Specialty Insurance. The Real Cost of Being Underinsured: A Family Entertainment Center Case